Changing times (or, why is every layoff 10-15%?)

Changing economic markets suggests a shift in how some companies should operate, as well as what risks to assume for 2023

First, some recent history…

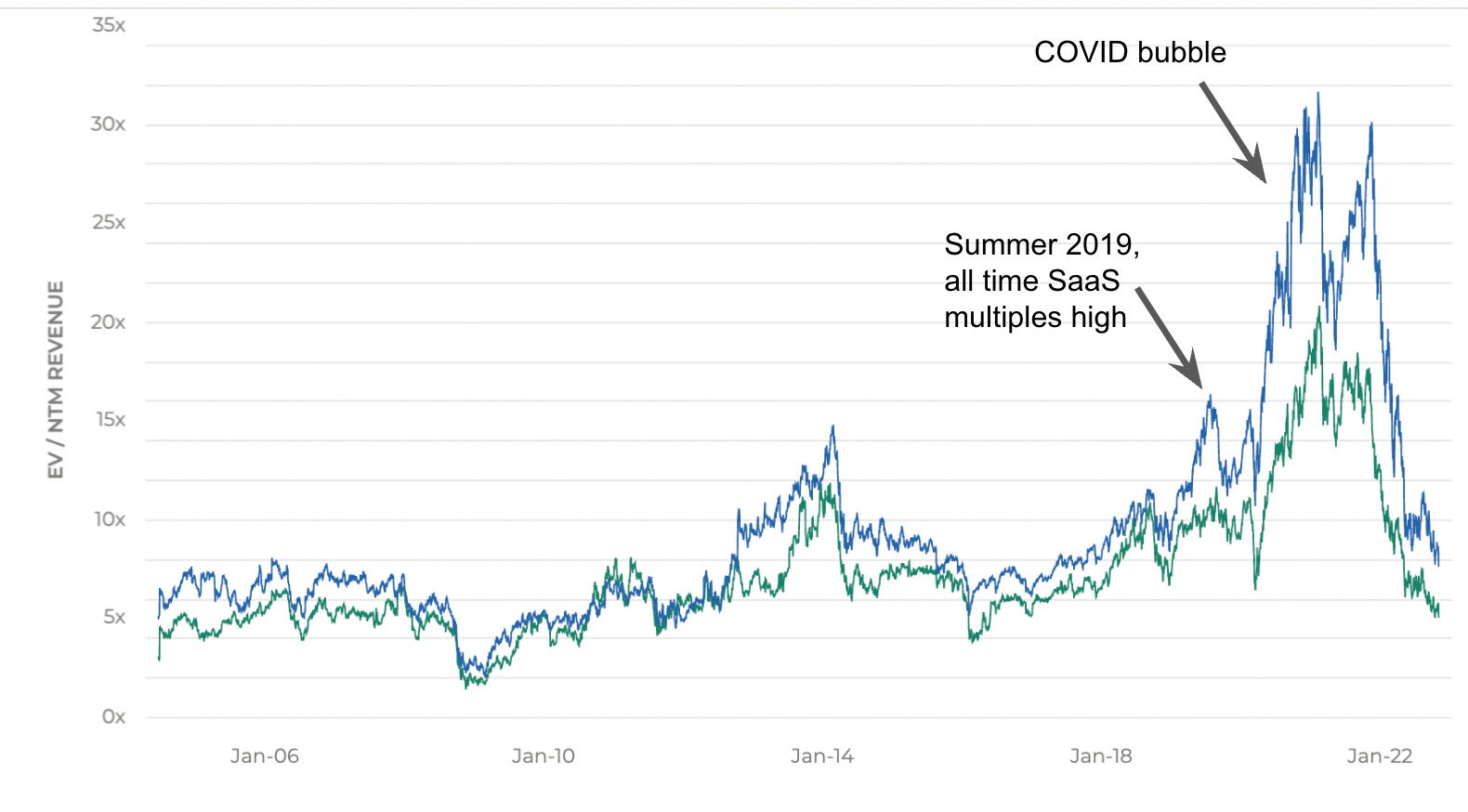

In 2019, tech and software multiples hit all times high. After 10 years of quantitative easing and lowered interest rates, many did no think tech company multiples could go any higher.

Then COVID hit and the government took unprecedented monetary policy action by dropping interest rates to ~zero, expanding the federal balance sheet by buying assets, and printing trillions of dollars to provide money drops to large swathes of the US population affected by the rushed and unprecedented COVID lockdown policies. A number of these macro financial engineering approaches continued even post COVID-vaccine rollouts, raising questions on what motivated them.

Zooming in on the COVID era it is clear valuation multiples for public tech were out of line with historical norms. (Previous chart from Meritech, some of the slides in this post from Battery):

Interest rates are typically inversely correlated with the multiples ascribed to growth stocks - as these stocks are often valued on future discounted cash flows, and the discount rate ascribed drops (or grows) with the interest rate. Interest rate policies led to out of band high tech multiples across SaaS, fintech, consumer and other areas.

In parallel, the lock downs drove ecommerce and other technology adoption - if you are stuck at home, you are more likely to order food via an online app. If you are airdropped money by the government, you are likely to spend at least some of it (which was indeed a partial purpose of the money drops). Once you are released from home and fear[0], and go see friends, it turns out your online spending snaps back closer to the longer term trends.

As you can see in the chart below, interest rate changes anti-correlate with tech stock multiples. The lower the rate, the higher the tech multiple. A zero interest rate environment led to massive upswings in tech multiples. Money being pumped into the system also allowed companies to pay a low cost of capital to fund inefficient growth.

Given massive multiples, revenue growth driven in part by government stimulus, money drops, and low cost of capital, tech companies went on hiring binges.

For example, Alphabet ended Q3 2022 at 186,779 employees, 2X the size of January 2019. Meta ended Q3 2022 with 87,314 employees, up >2x Jan 2019. Meta has just announced an 11,000 person layoff, returning the company to (checks notes) 5-7% bigger than January 2022.

These tech hiring binges were not limited to big MAMA (Meta, Alphabet, Microsoft, Apple) companies. Small startups, often pre-product market fit but backed by enthusiastic venture capitalists, frequently hired rapidly ahead of revenue and traction. In the past a $1M ARR company would often have 5-20 employees. During COVID, some companies ballooned their employee counts regardless of revenue (in one example a company reached almost 400 employees on less than $1M in revenue before shutting down in 2022). It was not uncommon to see companies with $1-2 million in revenue raise $100 million at a $1 billion valuation and hire a 100 to 150 person team.

The $1 billion valuation on a few million in revenue contrasts sharply with pre-COVID public market norms of needing ~$100M in revenue for every $1 billion in public market cap. This led to many private unicorns being minted during COVID, in some cases with low revenue, per the below chart from Battery.

In parallel, anyone who follows history knows that roughly anytime you print and handout money, you get inflation [1].

Given that many governments coordinated their actions, inflation was not limited to just the USA. Below is, as an example, Germany from the NYTimes.

High inflation creates all sorts of issues, and as such the Fed (and other countries equivalents) are raising interest rates in an attempt to curb inflation. (As an aside, the last time we dealt with inflation the Fed Chairman at the time, Paul Volcker raised federal funds rates to ~20% to quash it! We are only at ~4% today).

Since higher interest rates correspond with lower growth company multiples, ongoing interest rate hikes in 2023 might (1) drop tech multiples further (2) slow revenue growth for companies as capital in the markets tighten and (3) potentially push the US into a recession that will further slow spend (and therefore company growth).

Indeed, the goal of the rate hikes is to push down demand and increase unemployment in order to drop wage and price growth. Assuming the Fed sticks to its guns the economy should cool substantially 2023.

In sum, the macro environment today is very different from that of last year, and should create onward downward pressure on tech companies and their multiples. (As if you need any further evidence, even Softbank presentations are going to get more boring.)

What is coming in 2023 for private tech

The most likely scenario for 2023 is a much worse macro environment than 2022. If 2022 is the hangover after the party where you are still a little drunk but have a headache, 2023 may end up more akin to accidentally driving your car into a tree. The most likely outcome is more interest rate hikes globally, a recession, and the first real wave in this cycle of private tech company failures, deep layoffs, down rounds, M&A, and other activity.

Denial isn’t just a river in Egypt

In general, some companies still seem to be feeling optimistic relative to the pending environment. Many of them raised 3-4 years of cash when it was available and assume they will grow into lofty valuations. Layoffs for most companies are all oddly within the same band of 10-15%, few private tech companies seem to have a “recession scenario” as one of many scenarios in their financial plan in 2023, and some seem to think capital will be readily available for them if all else fails. For a subset of companies, this is likely to be wishful thinking.

Layoffs

A number of companies have started to do, or plan, layoffs. While not every private tech company should be laying off people (indeed some should probably be investing in growth including most pre-seed and seed companies), many later stage companies are likely over staffed (see MAMA company data on Meta and Alphabet in sections above). In general, it is better culturally and performance-wise to overcut, assess, and rehire, then undercut and then do sequential layoffs.

Oddly, almost all companies that are doing layoffs seem to be planning a 10-15% layoff. This feels mimetic in nature. Every company is different, has different headcount, burn, growth, margins, etc yet all magically converge to the exact same layoff %.

10-15% seems to be the number that reflects “big enough that I can tell myself and my investors or board I am doing it, but not so big that it causes truly uncomfortable conversations for the team”. Please don’t misinterpret this prior statement- undoubtedly many companies should cut exactly in the range of 10-15%. However, some should cut 5%, or maybe even grow, while many should probably cut 30, 40, 50% or more. For example, during COVID Airbnb cut 25% of its team. One venture firm I know is encouraging companies to assume they should cut 50% and then use financial modeling to prove otherwise.

Eventually, companies that should cut 40-50% get there - it often just takes 2-3 cuts at which point a lot of cash has been burned and company culture is hurt by the sequential nature of it all. Many companies that could have cut 50% up front end up spiraling down due to consuming too much cash between cutting 10% and realizing another 40% should be laid off to reflect the economic reality of their business.

One thought exercise a company planning a RIF can do is imagine a scenario with a 25-50% headcount cut. How does that really impact team output and burn? What teams would you be forced to cut and how much do those teams really truly matter? How does that align with your various financial scenarios? Even if you still only cut 10-15%, it might be an informative exercise.

The key thing to remember is that if your valuation is very far ahead in this new market environment, and your business slows due to recession or spending cuts, it may be hard to raise money in the near term. Layoffs should either get you to default alive (aka enough money to last reasonably indefinitely) or default fundable (a strong enough situation to be able to raise more money in today’s or tomorrow’s market). Things are likely to get worse before they get better. Make every dollar count.

Recession plans

Few private tech companies have a “recession plan” scenario for next year. Many are assuming a downside scenario in which growth may slow, but still be quite strong (e.g. 2.5X growth instead of 3X). For some companies this scenario may hold, but for many it is false hope which is preventing layoffs, M&A, or other activities.

One approach some companies are taking is to model out major customers by revenue and predict what may happen to each one. Or executive teams can look at early indicators of churn, accounts shrinking, or new business adoption slowing. While growth within a certain burn multiple is always good, the venture market is now unenthusiastic about growth with a high cost structure. When doing scenario modeling companies can also add a true “bad year” scenario amongst others, just to understand relative cash consumption with current team size or other assumptions.

In general, during market resets larger enterprise companies are the most stable customers, while startup customers and small businesses are the least stable as customers.

Fundraising & free rounds

Capital has had unheard of availability in the past few years and venture funds are bigger than ever. Many founders seem to believe that the worst case future fundraise is a down round or structured round. In reality, the true worst case is that you are unable to raise money ever again. Many companies will go out to market and realize that roughly no one wants to fund them after they burned $50M to get their current relative progress.

During the COVID era, due to pre-emption and excess capital, many companies raised at least one “free round”. In other words, many companies received a bolus of money 12-18 months before they would have historically been able to based on progress and traditional valuation metrics. For example, if you raised a $50M series B in 2022, perhaps you were only really at the $10M series A or seed stage relative to historical norms.

One exercise companies can do is imagine you never raised your last round. Deduct that dollar amount mentally from your bank account. How would this change your plans today? How would you operate differently? In some cases, this may actually be the way you should be operating your company (team size, growth targets, etc) today.

Either way, in 2023/2024 there will likely be many failed fundraises. The “free round” gives companies extra runway to operate. However, total capital raised will be used to measure how well you did on all the money you received already, and will be used by the market to judge if you would make good use of future money.

For later stage companies you need to imagine how to get to default alive (profitable or close to it), or default fundable (strong metrics and capital efficiency) on the money you already have.

Culture & mission resets

During good times, some companies may lose some aspects of their frugality, results orientation, customer-centricity, operational excellence, and sense of mission. A number of companies are using this moment in time to reset culture more broadly to return to a more tightly run and higher functioning, leaner organization. Expectations for employee performance are going up, and a lot of the unnecessary accoutrements of excess capital are being dropped.

In parallel, many companies have had their mission drift during the Trump years and COVID. Rather than founder-led customer-centric mission orientation, companies drifted into a number of other arenas often driven by a small proportion of their most vocal activist employees. Shopify, Coinbase, and other companies have done resets on their missions, realigning their employees back to the basics of why the company exists and the company-specific mission.

One mental exercise a founder or team can do is to imagine how you want to shift your culture in lieu of the current world. What would you change? What would you emphasize more or deemphasize? How much focus do you want on frugality, hard work, leaner operations? How do you want to shift the company’s mission or things employees concern themselves with day to day at work? Where should the mental energy of the team go?

In general, tougher times lead to leaner staff and a tightening of operations, culture and mission. The back drop of layoffs, stock market shifts, and potential recessions make tough things easier to do by executives, and easier to be understood and agreed to by employees. CEOs who miss the current opportunity to reset culture & mission in the coming months may regret it years later. Now is the time to act.

Remote work

Anticipate more mid-size and smaller companies will go back more fully into the office as times get tougher. This will not be one size fits all, but will be an increasing trend.

As CEO now is your opportunity to rethink remote work. You may decide you want to continue as is, or you may want to make changes. You have an opportunity to act.

M&A

M&A activity has picked up dramatically over the last few months, from roughly no activity in the last 3-4 years. M&A is picking up as founders either realize that they do not have as strong of a path on their own as they once thought, they are unable to fundraise, or as a buyer they realize there are strong assets they can buy into their company.

M&A should only accelerate in 2023. Founders of companies considering selling may want to front-load it to the beginning of next year as 2023 should eventually have a flood of people wanting to exit, given an ever worsening environment. Supply and demand in the M&A market is likely to shift strongly.

Offense

If you are a company in strong shape (capital efficient growth or profitability, robust customer renewals and NRR, lean team and strong culture etc.) - how can you use the environment offensively? What unique good people can you hire in an increasingly stark employment environment? Who should you go buy? Can you still make your team leaner and more efficient and up the bar on performance expectations? Can you refocus culture or mission?

Many companies have a market cap a few years ahead of current metrics. How can you use your stock offensively? (M&A, hiring, etc).

Summary

COVID era policies and loose monetary policy led to hiring excesses, inefficient capital expenditures, and inflation. Inflation has led to interest rate hikes, which if sustained will continue to crunch tech multiples, capital availability, and will overall tighten the screws on private tech companies. The most likely scenario is 2023 will be a much tougher environment for startups than 2022. CEOs and executive teams should consider planning accordingly.

There is an old saying that you should never waste a good crisis. Now is a time for CEOs and their teams to give themselves permission to toss out old assumptions about their company, mode of operating, growth targets, team, culture and mission. There will be few opportunities to make big changes like in the current environment.

Summary of exercises mentioned

For some companies, none of these exercises apply. I am not suggesting everyone do these, but you may consider one or more of the below if applicable to your current status.

Scenario modeling. For at least one of your financial forecasts include a true worst case recession plan. How does this impact cash needs, headcount etc? Going through your major customer list and available information about them (revenue, layoffs, spend targets etc) - how does their future impact spend with you?

Layoffs. If you are planning a layoff, imagine what a 30% or 50%+ cut would look like for your company (even if you are planning for 10-15% per mimetic action). How does this tie into financial scenarios above? What teams would you be forced to cut and how? What would your organization look like if you were forced to do a deep cut up front? What “untouchable” aspect of your business would you need to jettison?

Free round. Imagine you never received your last round of funding (if it was far ahead of your progress). Mentally deduct that money from your budget. How would you operate your company differently? This does not mean you need to make any changes, but it may force different thinking and reflect your company stage. Of course, you can also imagine how to use that extra capital to self fulfill market cap & get more aggressive in the market as well.

Culture reset. What is the right company culture and mission for todays environment? What do you want to change? Where do you want your teams mental energy and cycles to go? How would you communicate these changes to your team?

M&A. Should you sell the company? If so, to who and when? What would trigger a sales process for you? If you plan to buy companies, make the list of targets and prioritization. Next year will be a good year to buy others. Late in 2023/early 2024 may be increasingly hard to sell if the market gets saturated with M&A opportunities.

Remote work. What is your ideal work setup, ignoring the risk of people quitting or employee pushback? How can you go about implementing your ideal?

NOTES

[0] Exempting the Bay Area and other areas, which seem to continue to include masking, warning signs, plastic barriers and other COVID era vestments and hierograms of the anxiety-safety industrial complex.

[1] Going in the midterms, the White House took the initiative to push down inflation by selling off strategic oil reserves to dampen the impact of energy prices on inflation. Since energy is an input into everything else, lowering energy prices should cause inflation to dip. The strategic oil reserves are limited and the sales are not sustainable. This might be under-discussed in the context of current inflation rates and the ongoing need for interest rate action.

MY BOOK

You can order the High Growth Handbook here. Or read it online for free.

OTHER POSTS

Markets:

Startup life

Co-Founders

Raising Money

Old Crypto Stuff: